The 5 Best Educational Plans in the Philippines

How we picked

Cost of Premium

We picked plans with reasonable premiums for you in the long run. We considered how you would need to balance your finances, while choosing the best for your kid.

Investment Vehicles

We studied the investment vehicles used in the educational plans. We got you the best investment vehicles capable of making the most out of your premiums once your child goes to college.

Conditions

For us, the contents of the educational plans best show how you invest for your child’s future. We included checking the coverage of your premiums and insurance add-ons.

Company Reputation

Having an educational plan mostly requires a minimum of 5-year investment, some requiring more. Long-term investments require trust, so we chose reputable insurance companies in the Philippines for our recommendations.

1. Manulife Education Builder

Coverage: 4-year College or 5-year College

Cost of Premium: Php 20,000 (Regular Pay), Php 40,000 (10 years), Php 50,000 (5 years)

Education Benefit: Php 100,000 to Php 150,000 (Minimum Annual Benefit)

Time horizon: 5 years, 10 years, or more

Add-ons: Manulife Affluence Builder

| Cost of Premium | 4/5 |

| Investment Vehicles | 5/5 |

| Conditions | 4.5/5 |

| Coverage | 4/5 |

| Add-ons | 5/5 |

| Company Reputation | 5/5 |

Pros

- Suited for college education investment only

- Flexible payment schemes

- Life insurance

- Waived premiums for accidents or death

- Access to Manulife’s investment funds

Cons

- Additional expense due to insurance

- Incidental Fees

- Fund Management fees

- Minimum withdrawals

- Maintaining balance

Manulife Education Builder provides you with a holistic educational plan not only guaranteeing your child’s education. It also secures your child’s education if something unfortunate happens to you.

We recommend the Manulife Education Builder for those who need flexible payment schemes and guaranteed payouts. The guaranteed payouts can be accessed when your child goes to college, or should you experience permanent disabilities or death.

We liked how the plan allows you to have different annual premiums for flexibility and budgeting.

The minimum you can get is a 5-year premium. We think this is a good value as you can pay your premiums annually for 5 years,and then reap those benefits in the future.

You just need to wait until your child gets to college before you can get your benefit. We suggest you keep adding more premiums even after your 5th year for more gains.

In fact, we think the Manulife Education Builder encourages you to start saving early to give you time to grow your premiums. The latest you acquire this plan is when your child is 10 years old.

Also, investing in Manulife Education Builder provides you access to Manulife’s investment funds.

We think of this as a huge plus because it provides you access to profitable companies around the world.

Although we love Manulife’s educational plan, we disliked how much fees are included in the package. They even have a maintaining balance when you choose to withdraw your funds.

We think you can offset these fees when you stick to paying your premiums and invest for more than 5 years. However, we also suggest you to balance your finances with paying your premium.

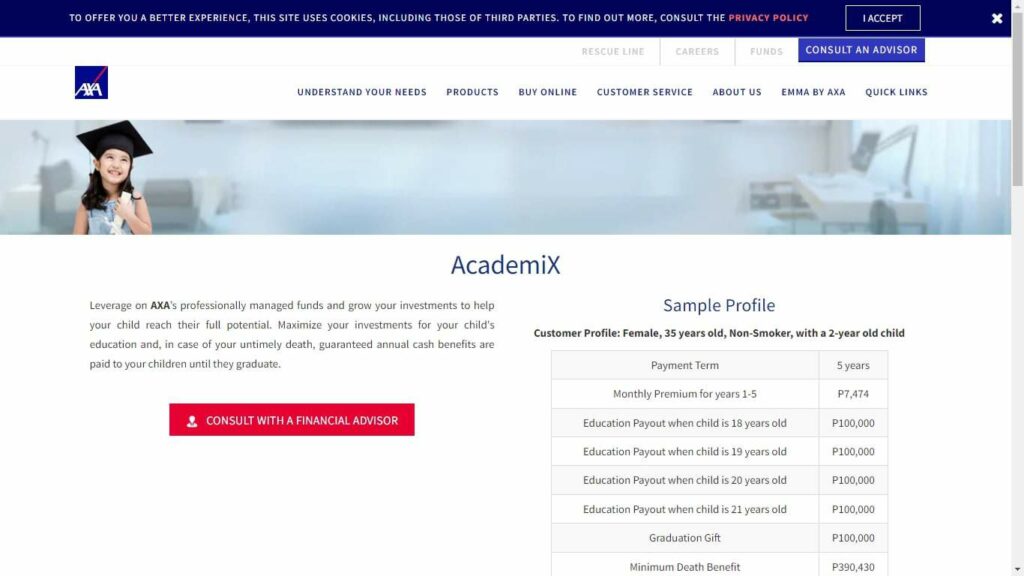

2. AXA AcademiX

Coverage: 4-year College

Cost of Premium: Depends on your policy

Education Benefit: Depends on your policy

Time horizon: 5 years, 10 years, 20 years, or more

Add-ons: Life insurance (optional), Permanent Disability (optional)

| Cost of Premium | 5/5 |

| Investment Vehicles | 5/5 |

| Conditions | 4.5/5 |

| Coverage | 5/5 |

| Add-ons | 4/5 |

| Company Reputation | 5/5 |

Pros

- Cash graduation gift

- Top-tier investment vehicles

- Education-centered plan

- 10th and 20th anniversary Loyalty Bonus

- Optional Life Insurance

Cons

- Alternative investment vehicles exist

- Only covers 4 years of college

If you are looking for an education-centered plan, then we cannot recommend AXA AcademiX enough.

We liked how it allows you to focus only on investing in education. Because the insurance policies are optional, you can invest or use your money for other expenses.

AXA’s fund is managed by Metrobank Trust Banking Group.

They are one of the best fund managers in Asia, and we approve of their long-term investment performance. We think they are more than capable of making sure your fund stays secure while it grows.

AXA also gives you a 10th year and 20th year bonuses when you keep investing with them. We love how this encourages you to save money early, and incentivizes your stay with them.

And the incentives do not end there. Perhaps the best and unique part of this educational plan is how it gives your child a graduation gift!

The graduation gift is equivalent to the payout period AXA gives back to you during the college of your child. We think this is a great way to stay motivated in terms of payments.

What we did not like about this product is how it feels very similar to investing.

While investing is what education plans should do, this makes us feel you can still screen for other investment vehicles. In fact, we think you can even diversify your portfolio more with other investment vehicles.

You can even get lower management fees or lower minimum monthly deposits compared to paying higher annual premiums.

Lastly, the plan only covers 4 years of college education. Although not emphasized, AXA does not encourage anything about continuing to invest in this plan once your child graduates.

3. AIA Future Scholar

Coverage: Education, Life insurance, Disability

Cost of Premium: Php 20,000 (Minimum Annual Premium)

Education Benefit: Depends on your contributions

Time horizon: Minimum of 5 years

Add-ons: Life insurance (optional), Disability benefits (optional)

| Cost of Premium | 5/5 |

| Investment Vehicles | 4/5 |

| Conditions | 4.5/5 |

| Coverage | 4/5 |

| Add-ons | 5/5 |

| Company Reputation | 5/5 |

Pros

- Affordable premium

- Flexible premium allocations

- Optional life insurance

- Optional disability benefit

Cons

- Php 20,000 yearly premium can only be paid annually

- Private investment vehicles

- Payment policy not guaranteed

AIA Future Scholar will provide you with the cheapest annual premiums available in the market.

We recommend this for parents who have been hesitating to invest on educational plans because of cost premiums. We think this may change their minds rather than insisting on putting their money on their savings.

A Php 20,000 annual premium is a very affordable educational plan premium. We think this suits young families who might struggle paying larger amounts.

However, take note that the Php 20,000 premium can only be paid through annual payments.

You will need to contribute at least Php 30,000 for the monthly, quarterly, and semi-annual payment methods.

We also loved how the fund allows flexible fund allocations. Being able to manage your money earns a huge plus on our review.

You can choose to have a 50-50 option or 20-80 option.

The 50-50 option evenly divides your premiums into guaranteed savings and investments. The 20-80 option puts 80% of your premiums to investments and 20% to guaranteed savings.

Then, you can purchase a separate optional life insurance and disability benefits. We think this works best with a cheap annual premium.

You can later choose to have the optional life insurance and disability benefits once you have a bigger budget.

While we think of cheap premiums as a plus, AIA’s policy reveals that your education benefits may not be guaranteed.

We suggest investing for a longer time horizon or paying more premiums to be able to grow your money.

Also, we question the strength or performance of the investment vehicles of the AIA Philippines.

They do not mention the funds or the fund managers involved in investing your money. We value where your money goes, especially for large investments such as education.

4. Sun FlexiLink by Sun Life

Coverage: Education, Retirement

Cost of Premium: Depends on your policy (can be increased anytime)

Education Benefit: Depends on your policy

Time horizon: 10+ years

Add-ons: Life insurance, Disability benefits, Accidental Death Benefit , Critical Illness Benefit

| Cost of Premium | 5/5 |

| Investment Vehicles | 5/5 |

| Conditions | 4.25/5 |

| Coverage | 3.5/5 |

| Add-ons | 5/5 |

| Company Reputation | 5/5 |

Pros

- Reputable Investment vehicles/ company

- Critical Illness Benefit

- Can be used for education, retirement, and other life milestones

Cons

- Invests in equity

- No minimum payment scheme

- No guarantee on returns

- Not education-centered

If you plan to pay premiums for more than 10 years or for a longer time horizon, then this is the education plan for you. We recommend Sun FlexiLink by Sun Life for those looking for long-term gains with insurance.

We recommend this plan for breadwinners looking to safeguard their family’s financial well-being.

The insurance that comes with this product allows you to stay focused on paying your premiums without worrying about your loved ones.

No other educational plans offer this extensive set of insurance you can use when something happens to you.

To prove our point, the plan can offer you up to Php 1,000,000 in benefits, as long as you pay your premiums based on your policy.

We think this gives you peace of mind in the long run, especially when you are still in the early stages of building your wealth and educational fund.

What we don’t like about this product is how it uses equity investments.

In investing, this is only considered for high risk investors. Even Sun Life does not provide a guarantee on you giving your premiums gains if the market does not favor you.

Hence, we recommend you ride with them on the long term. If you are able to stick with their premium, you might also transition your investments into a retirement plan after funding your child’s education.

However, if you are only looking for an education-centered plan, we suggest you screen for other educational plans. We suggest you opt for a plan that makes life insurance optional.

5. Insular Life Wealth Assure Plus Education

Coverage: Education

Cost of Premium: Depends on your policy

Education Benefit: Depends on your policy

Time horizon: 10+ years

Add-ons: Accidental Death Benefit, Premium Benefit, Critical Illness

| Cost of Premium | 5/5 |

| Investment Vehicles | 5/5 |

| Conditions | 4/5 |

| Coverage | 4/5 |

| Add-ons | 4/5 |

| Company Reputation | 5/5 |

Pros

- Waived premiums for accidents

- Renewable term insurance

- Many investment vehicle options

- Compressed payment option

- Php 500 minimum monthly investment top-up

Cons

- Long time horizon

- Paying period not guaranteed

The Insular Life Wealth Assure Plus Education is for you if you have investing experience and would like to apply it to your child’s educational plan.

We were impressed with the vast investment vehicles they offer. You can feel comfortable investing with Insular Life whether you are a conservative or risky investor.

What feels equally impressive for us is how it only has Php 500 minimum monthly investment! This top-up makes your investment affordable and can lower your monthly premiums.

Another thing we loved about this educational plan is its renewable term insurance.

We think of this as something you can take advantage of. It does not force you to mix life insurance with your child’s educational investments.

Rather, you are able to avail their waived premium rider option. This allows your premiums to be paid in full in cases of accident or death.

The Insular Life Wealth Assure Plus Education has a compressed payment option for short-term educational goals.

We find this unique as other educational plans only focus on long-term gains. Of course, you can also extend it as long as you’d like, such as your child’s graduate studies.

Despite that, we still think of this to be more effective for the long-term horizon.

Insular Life provides no guarantee for your payment period. We recommend you to invest long-term while enjoying flexible payment options when paying for your premiums.